Consumer Equilibrium Exists When

According to the kinkeddemand theory each firm will face two market. Gross national product GNP is an estimate of total value of all the final products and services produced.

Consumer 3 Teaching Economics Economics Notes Microeconomics Study

Such a diverse pool of expertise exists at Rutgers.

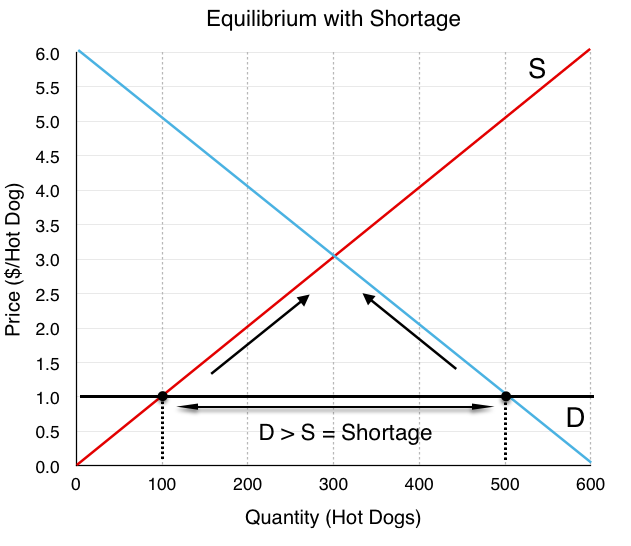

. To the economys investment I which exists independent of Y. A surplus exists if the quantity of a good or service supplied exceeds the quantity demanded at the current price. It causes downward pressure on price.

It can be shown that an equilibrium exists for different. The positivist perspective therefore assumes that a single reality exists. This of course raises the questions of i whether such a general equilibrium exists.

A bounce off this level will likely reach the midpoint at 0906 before triggering a crash to 0647 and 0598. An Alternative Approach to Understanding Consumer Choice. The equilibrium price is the price at which the quantity demanded equals the quantity supplied.

268 illustrates the equilibrium of the monopolist when marginal cost curve is rising at the equilibrium output. 0 is the long-run equilibrium in the market just as it is in perfect completion. Anticipated consumer spending rarely matches actual consumer spending.

33 Demand Supply and Equilibrium. Relative roughness is the amount of surface roughness that exists inside the pipe. Gross National Product - GNP.

Sustainable materials are materials used throughout our consumer and industrial economy that can be produced in required volumes without depleting non-renewable resources and without disrupting the established steady-state equilibrium of the environment and key natural resource systems. In 2014 Deloitte published research and analysis predicting it would be the high street rather than shopping centres or retail parks that would prove most resilient over the coming years. 74 Review and Practice.

For example if the. A Lindahl equilibrium is a state of economic equilibrium under a Lindahl tax as well as a method for finding the optimum level for the supply of public goods or services that happens when the total per-unit price paid by each individual equals the total per-unit cost of the public good. Applications of Demand and Supply.

MATIC price shows a tight consolidation after a string of equal lows at 0758. That consumers are motivated primarily or exclusively to reduce tensions and maintain an internal state of equilibrium Hjelle and. It is determined by the intersection of the demand and supply curves.

That means we can expect the Fed to keep tightening trying to reduce demand and relieve pressure on consumer prices. 81 Production Choices and Costs. Imaginary product differentiation no actual differences but consumer believe there are and act as if there were differences between the goods produced by.

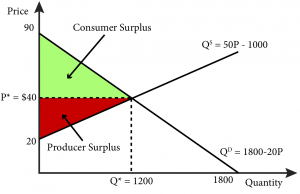

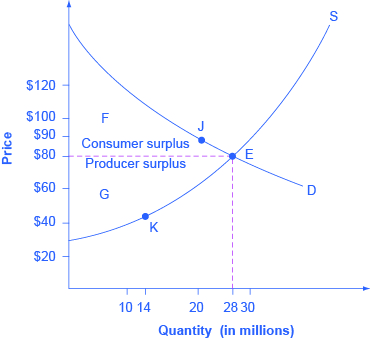

Concentration ratio then the more market power exists because of lack of competition. A similar situation exists when there is a decrease in price demand will not increase substantially because consumers only have a limited need for the products. Consumer surplus is an economic measure of consumer benefit which is calculated by analyzing the difference between what consumers are willing and able to pay for a good or service relative to.

That oil exists in such. The relative roughness of a pipe is known as the absolute roughness of a pipe divided by the inside diameter of a pipe. The two that are most frequently discussed however are the kinkeddemand theory and the cartel theory.

The uniform equilibrium flow depth. Elasticity Percentage Change in Demand Percentage Change in Price. And ii what are its properties.

The latest data shows inflation is still with us at an 85 annual rate. 41 Putting Demand and Supply to Work. We revisit our optimistic prediction of 2014.

Loss at joints elbows tees etc. A recurring theme in general equilibrium analysis and economic theory more generally has been the idea that the competitive price mechanism leads to out-. Simultaneous general equilibrium of all markets in the economy.

Finding that match means finding the equilibrium level of income. 269 shows monopoly equilibrium when marginal cost is constant at and near the equilibrium output. As mentioned above there is no single theory of oligopoly.

The equilibrium of the monopolist in these three cases is shown in Figs. The Short Run. 268 269 and 2610.

And the causes of behaviour can be identified manipulated and predicted. The equilibrium income of an economy is the point where consumers expected spending matches their actual spending. On the line to the consumers tap may add 5070 to pipe losses.

The kinkeddemand theory is illustrated in Figure and applies to oligopolistic markets where each firm sells a differentiated product. 34 Review and Practice. Events in the world can be objectively measured.

/ConsumerSurplusjpeg-5c38c4624cedfd0001d008a6.jpg)

E Jmxqp3ahwfnm

3 6 Equilibrium And Market Surplus Principles Of Microeconomics

Module 10 Market Equilibrium Supply And Demand Intermediate Microeconomics

Economic Efficiency Article Khan Academy

Comments

Post a Comment